ICSANA

Abstract

In wake of technological advancements energy is becoming focus of economic development. India neighbouring China and Pakistan is an emerging regional economic power. India has bolstering and dynamic economy with increasing needs of energy. The conventional indigenous energy resources are just not enough to meet its needs, whereas GCC countries are endevoured with conventional resources of energy in form of oil and gas. This paper critically analyzes the role GGC countries can play in meeting India’s Energy need. The paper also examines the potentials and available options India can exploit to meet its energy needs through alternate routes.

Key Words: Energy, Energy Mix, Alternate Energy, IPI. TAPI, Shale Gas, GCC

Contents

1. Introduction

1.1 Methodology

1.2 India’s current state of energy resources

1.3 Available energy alternatives for India

1.4 The shale factor: implications for India and GCC

2. GCC’s Energy outlook

2.1 Saudi Arabia

2.2Kuwait

2.3 Oman

2.4 Qatar

2.5 United Arab Emirates

2.6 Bahrain

3. India’s future energy concerns and possible GCC role

4. Political and strategic concerns

4.1 Saudi Arabia, Iran and India’s energy needs

4.2 IPI or TAPI?

5. Some Recommendations

6. Conclusion

Bibliography

1. Introduction

India is second most populous country of the world after china. India shares its borders with emerging global power China and Nuclear Pakistan. According to the International Energy Agency (IEA), global energy demand is expected to grow by more than one-third over the period to 2035 with China, India and the Middle East accounting for 60% of the increase (Commission, 2013). In geo-political and historical context India has emerged as regional economic power and is likely to climb the ladder very fast in years to come as India has second fastest growing market for energy as well. India is projected to become the fourth largest economy in the world by 2020, after China, the United States (US) and Japan and its energy demands are likely to grow exponentially (Roy, 2014). With current growth rate and presumably the most populous country of the world by 2050 India needs to produce 800,000 MW of energy compared to current 160,000 megawatts.

India has been dependent on imports to meet most of its energy needs and the country is expected to increasingly become reliant on imports of all forms of commercial energy, with total energy import de-pendency increasing to around 80% by 2031 (Leena Shirvastva, 2007). Gulf Cooperation Council (GCC) has six member countries namely Saudi Arabia, Bahrain, Oman, Qatar, united Arab Emirates and Kuwait. The Gulf Cooperation Council (GCC) has become a major trade partner for India as bilateral trade has grown tremendously. The total trade between India and the GCC has gone from about US$ 5.55 billion in 2000–01 to US$ 158.41 billion in 2012– 3. Such a massive growth during a short period of one decade can be attributed mainly to the higher commodity prices, especially oil prices, in that period, and partly to the increased efforts to enhance trade relationship that were undertaken during this period by both sides. Today, the United Arab Emirates (UAE) and Saudi Arabia are among the top five trading partners of India (Pradhan, 2014).

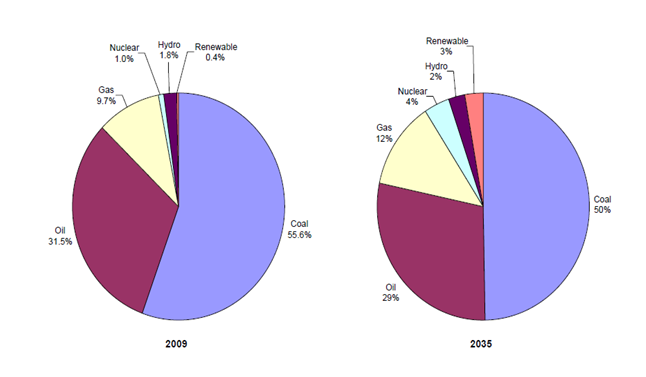

India has fourth largest coal reserves and id meeting more than 50% of its energy needs through coal but it is estimated that in coming 40-45 years India would deplete all it existing coal reserves if new exploration are not made. Natural gas, nuclear power plants and hydro power and other alternate energy sources are used to meet rest of the needs. India’s energy needs are expected to rise 3.01 % annually from 2009 to 2035 (Kumar, 2012)

Graph 01

Source: (Kumar, 2012)

Beyond economics and trade there are some long term sociopolitical and geostrategic and dimensions of energy demand and supply as well. It is important to note that most of GCC countries are Muslim monarchies and have strong strategic and trade ties with USA and Europe. Important question is; what alternatives India have to meet its energy needs? There are some sub questions as well attached to the major question:

- What possible role GCC countries can play in assisting India to meet its energy needs?

- What are the strategic implications for India and GCC countries for long-term mutual cooperation in energy sector?

- What possible role Iran, Pakistan, India (IPI) gas pipeline can play in securing energy and minimizing import costs for India while Iran is facing political and economic sanctions on its nuclear program by USA and Europe at present?

- In case of political instability in Arab world, how can India manage to establish trade routes to central Asian republics via Afghanistan through Pakistan?

1.1 Methodology

This is a uni-thematic multidimensional study. Secondary data in forms of research papers, reports, articles including news paper articles is collected. The interpretation and analysis of both qualitative an quantities data is primarily based on cross verification method.

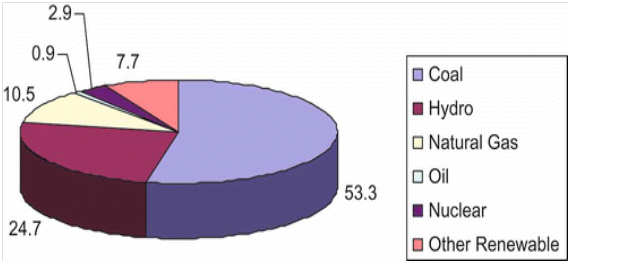

1.2 India’s current state of energy resources

To view the data in its real-life context, 25 percent of India’s populations 48 or 57 percent of India’s rural households have no access to electricity. India’s current power generation capacity is around 159.64 giga watt (GW) and the power requirement by 2031 is estimated to be 800 W. Coal is used for generating 53.3 percent of power and is followed by hydroelectricity which constitutes 24.7 percent. In addition there are also power cuts which are 13.3 percent at peak requirement.51 100 million households (more than 75 percent of India’s rural and 22 percent of its urban households) have no access to modern forms of energy and are dependent on biomass for household needs including cooking (Kumar, 2012).

Graph 02

Source: (Kumar, 2012)

The data given in above mentioned figure exhibits the optimum potential of India’s installed capacity to produce energy. Hydro power constitutes around 25% of energy output. Hydro power is a reliable source but in current climatic conditions and changing raining patterns the water flow in upland zones in expected to decrease consequently having a negative impact on energy production.

1.3 Available energy alternatives for India

India’s options for energy supply are limited. It has very small reserves of crude oil and currently nearly 80 per cent of consumption of petroleum products is based on imports. While some more reserves of natural gas have been located in the Krishna-Godavari basin, these deep sea reserves pose formidable challenges to exploit. Domestic gas is not expected to constitute more than 20 percent of India’s primary energy supply. Cellulosic ethanol, when the technology is developed can make a substantial contribution if ethanol can be produced from agricultural wastes such as wheat straw or rice straw. The sources that have sizable potential are solar energy and nuclear power. India’s strategy is to use its limited uranium reserves to run first generation plants that also produce plutonium along with power, using the plutonium in fast breeders reactor that produce more plutonium than what is put in, and then using in the third stage its abundant resource of thorium can provide 4 to 5 million MW of power for more than 100 years. The catch here, however, is the time required to realize this. By 2030 one can expect no more than 100 GW of nuclear capacity. (Parikh, 2011)

Reuters India reported in March 2013 that, besides heavy reliance on coal energy and having fourth largest coal reserves in the world India has imported 20% more coal from December 2013 to January 2014 , reason being the lowering coal prices in Indonesia and increase in value of Indian Rupee. Whatever the reasons may be matter of the fact is that coal may not be the long term option for India’s energy needs. India has to look in to alternate energy particularly solar and nuclear sector to meet its future energy needs.

India produces around 03% of energy from its current nuclear power plants and is expecting 08% enhancement in the capacity by year 2032.

The possible nuclear power capacity beyond 2020 has been estimated by Department of Atomic Energy (DAE) is shown in the table. In energy terms, the Integrated Energy Policy of India estimates share of nuclear power in the total primary energy mix to be between 4.0 to 6.4% in various scenarios in the year 2031-32. The study by the Department of Atomic Energy (DAE), estimates the nuclear share to be about 8.6% by the year 2032 and 16.6% by the year 2052 (S.K.Jain, 2012).

It is important to note that ‘other renewable’ energy contributes 7.7 % to total energy mix along with hydro power contribution of 24.7 %. In total hydro power and all renewable energy resources including solar and wind power together produce one third of the total energy. Preliminary assessment of the status of wind power development in potential states of India indicates that there should be a stable and uniform national policy to make wind power projects financially attractive across the country. CWET has recently updated its estimates for wind energy potential in India as 48.5 GW _as compared to the 45 GW before_; however, the Indian Wind Turbine Manufacturers Association IWTMA estimates indicate that the potential for wind energy development in India is around 65–70 GW. Therefore, for the large-scale penetration of wind energy in India it is critically important to assess realistic potential estimates and identify niche areas to exploit the wind energy resource (Ishan Purohit, 2009). Solar energy is another workable option to enhance India’s potential in meeting its energy needs.

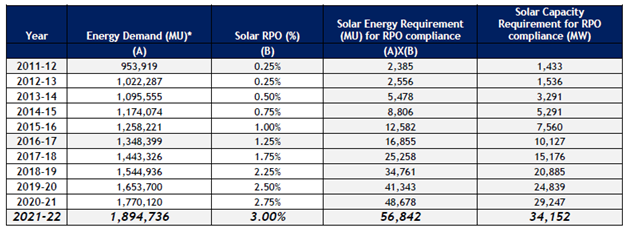

Table 01

Source: Ministry of New and Renewable Energy, government of India

Ministry of New and Renewable Energy, government of India on its official website has reported “Among the various renewable energy resources, solar energy potential is the highest in the country. In most parts of India, clear sunny weather is experienced 250 to 300 days a year. The annual radiation varies from 1600 to 2200 kWh/m2, which is comparable with radiation received in the tropical and sub-tropical regions. The equivalent energy potential is about 6,000 million GWh of energy per year”. Above mentioned table suggests that the planned installations for solar energy would produce more than thirty four thousand megawatts of electricity if yearly set targets are achieved and proper periodic expansion in solar energy projects is made as planned.

1.4 The shale factor: implications for India and GCC

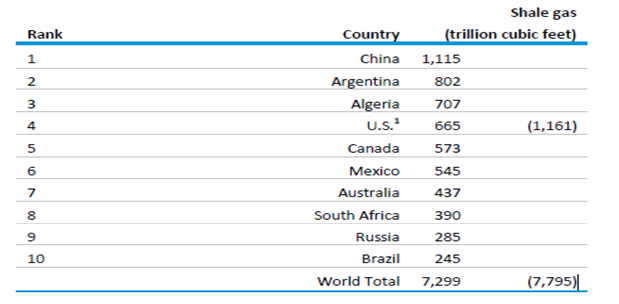

Though discovered in early 19th century shale gas is observing its boom since 1990. Experts are with the view that USA the leading energy consumer is paving the way for shale gas alternate natural energy source. Wind and solar energy hardware have high price of installation and maintenance whereas shale gas once explored in is far cheaper. Let us have a look on the top ten countries with recoverable shale gas resources (not reserves):

Table 02

Source: US department of energy

The table indicates that china is leading country with shale gas reserves. Though china has not yet put full muscle into exploratory efforts but it is projected that by 2020 shale gas would replace LNG in chins thus halting imports of LNG totally by china. Australia’s Macquarie bank and Germany’s Deutsche bank have already warned that Australian companies exporting LNG may face major export set back by 2020 (Jane Nakano, 2012). It should be clearly understood that data available on shale gas recoverable resources does not signify the assessment of reserves. Usually the success rate of extracted shale gas varies between 40% and 100%, depending upon the quality of gas and type of sedimentary rocks. In technical terms, out of world 95 basin India and Pakistan combine have six basin with shale reserves out with five are in India and one is in Pakistan which of course do not fall into top ten potential producers of the shale gas. Another important fact regarding shale gas investment by Indian companies that two major player of corporate India have heavily invested in shale gas ventures outside India. Reliance Industries took the lead and paid few billion dollars for 40-60% stake in various shale gas sources in USA. Bharat Petro Resources has also entered into an agreement with Australia’s Norwest energy to pick up a stake in two shale gas blocks from the Perth Basin. Other companies are also looking to invest in acquiring knowledge and assets (Deloitte, 2010).

Most important factor in considering shale oil and gas as an energy alternative is policy formation. USA, Canada, Australia and some South American countries have brought policy reforms in energy sector after introduction of shale gas a form of alternate energy. However Asian countries with larger proportion of energy consumption such as china and particularly India are far behind in bringing clear policy to exploit shale gas and shale oil as energy alternative. These policy issues are pertaining to training and expertise, taxation, regulation and environmental protection.

Wall street journal wrote “A shale-oil boom will help the U.S. overtake Saudi Arabia as the world's largest oil producer by 2020, according to the International Energy Agency, a shift that could transform not just energy supplies but also U.S. politics and diplomacy (Benoit Faucon, 2012).”

2. GCC’s Energy outlook

There are some interesting facts about GCC countries shared by US Energy Information Administration energy sector:

2.1 Saudi Arabia

- Saudi Arabia has almost one-fifth of the world's proven oil reserves, is the largest producer and exporter of total petroleum liquids in the world, and maintains the world's largest oil production capacity.

- Over half of its oil reserves are contained in only eight fields. The giant Ghawar field, the world's largest oil field with estimated remaining reserves of 70 billion barrels, has more proven oil reserves than all but seven other countries.

- Although Far East Asia is received an estimated 54 percent of Saudi Arabia's crude oil exports in 2012, Saudi Arabia still ranked second after Canada as a petroleum exporter to the United States.

2.2 Kuwait

- Kuwait holds the world's sixth largest oil reserves and is one of the top ten global producers and exporters of total petroleum liquids.

- Kuwait has implemented enhanced oil recovery measures to boost stagnant production rates. New discoveries have been made, but Kuwait's regulated oil sector hinders further exploration and production.

- Territorial dispute between Kuwait and Saudi Arabia led to the creation of the Partitioned Neutral Zone. Both countries divide equally the production of oil and gas in the zone.

2.3 Oman

- Oman is the largest oil and natural gas producer in the Middle East that is not a member of the Organization of the Petroleum Exporting Countries (OPEC).

- Enhanced oil recovery techniques helped Oman's oil production rebound from a multi-year decline in the early 2000s.

- Oman's total oil supply reached 924,000 barrels per day in 2012, and the government hopes to produce more than 940,000 barrels per day in 2013.

2.4 Qatar

- Qatar is the largest exporter of liquefied natural gas (LNG) in the world, and the country's exports of LNG, crude oil, and petroleum products provide a significant portion of government revenues.

- Qatar's crude oil production is the second lowest in the Organization of the Petroleum Exporting Countries (OPEC), but increasing production of non-crude liquids—most of which is a byproduct of natural gas production—is contributing to gradual growth in total liquids production.

- Natural gas is at the center of Qatar's energy sector. Already the world's largest exporter of liquefied natural gas (LNG), several recent developments in the country's natural gas sector could boost production in the short term.

- Nearly all of Qatar's natural gas production comes from the North Field, which is part of the largest non-associated natural gas field in the world.

- Qatar exports nearly 85% of its natural gas as liquefied natural gas (LNG), and it has been the largest exporter of LNG in the world since 2006.

- Despite rising electricity demand, Qatar had a surplus generating capacity of approximately 2.5 gigawatts, or nearly 30%, in 2012.

2.5 United Arab Emirate

- The United Arab Emirates is one of the 10 largest oil and natural gas producers in the world, and is a member of the Organization of the Petroleum Exporting Countries (OPEC) and the Gas Exporting Countries Forum (GECF).

- The United Arab Emirates is a major oil producer and exporter. In 2012, the country produced an average of 2.8 million barrels of crude oil per day, the eighth highest total in the world.

- The United Arab Emirates appears unlikely to meet a 3-million-barrel-per-day crude oil production target by the end of 2013. Further, the country may push back a longer-term 3.5 million barrel per day target until the end of the decade.

- The United Arab Emirates has one of the highest rates of per capita petroleum consumption in the world.

- The United Arab Emirates was the first country in the Middle East to export liquefied natural gas (LNG), and has exported more than 250 billion cubic feet of LNG annually, almost exclusively to Asia.

- The UAE is adding nuclear, renewable, and coal-fired electricity generating capacity, but currently relies primarily on natural gas.

2.6 Bahrain

- Bahrain’s refinery capacity far exceeds domestic crude oil production capacity. Bahrain has a 254,000 bbl/d export refinery at Sitra. Most of the feedstock is imported from Saudi Arabia, so that net exports for Bahrain are only about 5,000 bbl/d. Plans are underway to expand the refinery's capacity by 100,000 bbl/d by 2017.

- As with oil, the country is a small producer of natural gas, and produced 446 billion cubic feet of dry natural gas in 2011. In order to meet future natural gas needs, Bahrain plans to import gas from a number of sources, either via pipeline from Qatar or via imports of liquefied natural gas (LNG) following the awarding of a contract to construct a new LNG terminal.

Based on the data shared by US Energy Information Administration energy sector it can be deduced that except few variations GCC countries would continue relying on convention oil and gas resources as primary source of energy. UAE with more proactive approach is planning to meet energy needs with nuclear shale oil/gas resources. Abu Dhabi started building its nuclear reactor Barakah-1 in July 2012 (El-Katiri, 2012). There has been a debate on security issues related to establishment of nuclear power plant in GCC region. Saudi Arabia on other hand is planning to establish nuclear reactor for energy purposes. World nuclear Association on their website has reported that “A national Saudi Arabian Atomic Regulatory Authority (SAARA) has been set up to commence activities early in 2014. In May 2014 King Abdallah Center for Atomic and Renewable Energy (KA-CARE) signed an agreement with the Finnish Radiation and Nuclear Safety Authority (STUK) to assist in this by recruiting and training personnel and establishing safety standards”. Saudi Arabia is keen to add renewable energy to its energy mix. Primary consideration is to reduce domestic consumption of oil for energy purposes and enhance exports. James Burgess (Oilprice.com) reported that Saudi Arabia is planning to invest $109 Billion in solar energy project to reduce oil consumption and to add 30 percent of its electricity by 2032.

3. India’s future energy concerns and possible GCC role

India’s energy mix suggest that currently India is heavily relaying on coal as source of energy and in next four to five decades the Indian coal reserves are likely to deplete if utilized at current ascending consumption rate.

In a simple equation, keeping in view the current state of India’s trade and favourable political relations with GCC countries particularly with Saudi Arabia, United Arab Emirates and Qatar it is likely that GCC region would meet India’s energy needs in future as well. But there are two major concerns attached to this notion: 1. anticipating diminishing coal resources India’s gradual replacement of infrastructure accommodating petrol, diesel, LNG, shale gas, solar energy and Nuclear power plants. 2. India’s efforts to politically pave the way for international trade agreements facilitating oil/gas/coal/other energy imports and establishing new trade routes through neighbouring countries ensuring its energy security. UAE and Saudi Arabia are major international players in not only in oil and gas business but also are strong allies to USA.

As mentioned earlier in this paper large energy consuming countries such as China and Saudi Arabia in Asia, USA and Canada in North America and Australia have been making efforts to utilize alternate energy resources. It means there would be less pressure on conventional energy and prices would stabilize coming decade. In this scenario India has time, at least twenty years to gradually shift to renewable and alternate form of energy.

4. Political and strategic concerns

The major decision and policies on energy both by large producers and consumer have political implication on regional and world politics. The Organization of the Petroleum Exporting Countries (OPEC) is an organization of 12 oil producing and exporting countries, formed in 1960 for the purpose of regulating, contorting, and advising member countries on production, supply, and price stability for oil. The OPEC member countries accounted for 43% of all crude oil production in 2012. In addition, they hold more than 70% of all proven oil reserves in the world. The 12 OPEC members are Algeria, Angola, Ecuador, Iran, Iraq, Kuwait, Libya, Nigeria, Qatar, Saudi Arabia, the UAE, and Venezuela (Manging Oil wealth, 2013). It is important t note that out of twelve OPEC members six are from Asia and out of those six, four are GCC countries. The key decisions pertaining to energy or foreign policy taken by the governments of OPEC member countries can have long term strategic economic and political implications.

India has long history of trade, cultural and political ties with GCC region. People-to-people contacts have existed between India and West Asia for centuries. India has been a supporter of the Palestinian cause and has demanded a comprehensive relationship with the Palestinian state and the people. There are nearly 6.5 million Indians living and working in the West Asian region. According to a World Bank report India received US $ 70 billion in remittances during 2012 and a majority of the remittances came from the region. In addition, India’s total trade with West Asia in the year 2012-13 stands at US$ 205.71 billion. The region is also vital for India’s energy security. Nearly two-thirds of our hydrocarbon imports are from this region (Dr Arvind Gupta, 2014). Any political changes in Arab world especially in GCC region can have huge economic and political implications for India. India has 3rd largest Muslim population in the world. The history of pilgrimage and of trade Diaspora between Arab worlds and India is centuries long.

In the larger premises of discussion on India’s energy needs and GC role there are some other political factors to be taken into account that may Influence India and GCC

4.1 Saudi Arabia, Iran and India’s energy needs

Saudi-Iranian political relations are not ideal. In context of post Iranian revolution both countries have practices stagnant and cold diplomatic ties. Political analysts and experts of international relations suggest that the major reason behind tense relations between Iran and Saudi Arabia is not only the difference of school of thought rather historically other geopolitical and regional factors shaped their relations. Most important question is what is the positive/ negative implication for India’s energy needs?

According to Indian embassy in Saudi Arabia there are 2.8 million expatriate workers from India working in Saudi Arabia. For Saudi Arabia, India is the 5th largest market for its exports, accounting for 8.3% of its global exports. from News paper, The Hindu, reported (Oct 03, 2013) “Comparing Iran and Saudi Arabia in terms of Indian oil exports Saudi Arabia leads Iran.Iran was India’s second biggest oil supplier after Saudi Arabia in 2010-11. However, during 2012-13, it supplied only 13.1 million tones, lagging behind Saudi Arabia, Iraq, Venezuela, Kuwait and the United Arab Emirates. In 2011-12, Iran stood third with 18.1 million tons, against 32.5 million tons from Saudi Arabia and 24.1 million tons from Iraq”

It is also a fact that Indian is in better geographic proximity with Iran than Saudi Arabia but some experts take a radical position in analyzing the Iranian role in gulf and connect the trade to Iran’s nuclear program and possible conflict with USA and/or Arabs states. In the light of the increasing tension between Iran and the US, and Iran and Israel over its nuclear issue, the risk of this choke point being blocked has generated debate about Iran’s threat to shut down the Strait of Hormuz, and its implications for the energy supply for Asian and European countries. In fact, more than 85 per cent of the crude oil exports went to Asian countries like China, India, Japan and South Korea. Shutting Hormuz would block Qatar’s 77 mt a year of LNG production capacity, which amounts to 30 percent of global LNG supply. Such a scenario will increase the vulnerability of India’s supply from the West Asian region. Thus, to ensure its energy supply from West Asian region, India needs to promote the idea of laying oil and gas pipelines, bypassing choke points, to ensure uninterrupted energy supplies. Such pipelines could connect oil and gas fields in Iraq, Kuwait, Qatar, Saudi Arabia and the UAE to a suitable Omani port on the Indian Ocean (Roy, 2014). The other available and viable option for India is India Pakistan Iran gas pipeline (IPI) and /or Turkmenistan Afghanistan Pakistan India gas pipeline (TAPI). Some experts call it peace pipeline.

4.2 IPI or TAPI?

The proposed India Iran Pakistan (IPI) was initially India Iran pipeline. The gas pipeline was first proposed to be under 3000 meters undersea pipeline bypassing Pakistan. The survey conducted on project of II gas pipeline revealed that it may not be financially and technically feasible project. In 2005 Pakistan got involved through bilateral meeting with India and Iran and agreed to be part of gas pipeline. The 2700 kilometers pipeline is still under construction. That being said, there are several issues such as US-Iran tensions, Pakistan-India tensions, and Chinese and Russian interests that have caused delays in the construction of the pipeline and are currently complicating the matter. India itself backed out of the deal in 2008, almost 13 years after the conception of the pipeline deal. (Khan, 2012).

Turkmenistan-Afghanistan-Pakistan-India (TAPI) pipeline came into public notice when Turkmenistan, Afghanistan and Pakistan signed a pipeline pact in 2002 and India joined the project in 2006 (Abbas, 2012).

IPI or TAPI, India needs gas pipeline, but what is the political and strategic cost for that? Right from its inception USA and allied partner Saudi Arabia has opposed IPI pipeline but has supported the idea of TAPI. Both the projects are politically complicated for India particularly with reference to Pakistan’s as stakeholder. In the scenario of post American withdrawal from Afghanistan India is trying to relocate its role in Afghanistan whereas Pakistan not only borders Afghanistan but also has long history of influence in Pashtu speaking belt of Afghanistan particularly since cold war era and then during Taliban regime. Pakistan would like to safeguard its interest in Afghanistan after American withdrawal. Though India has shown renewed interest in IPI but still TAPI can put India in a strategically strong political and economic position.

5. Some Recommendations

- GCC countries are diversifying their energy mix; India should revisit its energy mix and come up with the comprehensive energy policy.

- If India can politically negotiate with USA and Saudi Arabia IPI pipeline may be a cheaper and viable solution to meet India’s some energy needs.

- India’s energy infrastructure requires modernization and overhauling. The changing energy mix would require restricting of the hardware and infrastructure as well.

- The new government of India after recent election in 2014 is likely to be a single party rule, giving more indolence in decision making and policy reforms/formation. If regional and international political conflicts are resolved particularly with Pakistan, India will be in far better position to expand its trade and meet its energy needs by Iran and central Asian republics.

- Indian companies investing in shale gas/oil in USA, Canada and Australia have opportunity to invest in Chinese shale gas projects as well. Should they invest there may be an opportunity for India to import gas from china in decades to come.

6. Conclusion

India is a large country with growing economy and energy is inevitably essential for its economic growth. GGC countries have strong and historical ties with India. The energy trade of GCC countries is likely to expand as they are investing more into nuclear and solar energy projects to meet their domestic needs and expand export of fuel. Remaining within framework of international nuclear law, India’s can share its nuclear expertise with Gulf States intending to install nuclear reactors for energy purposes. India has capacity and capability to politically pave its way for IPI and TAPI pipelines as these gas pipelines have great potential to meet India’s growing energy needs.

Bibliography

Abbas, S. (2012, April). IP AND TAPI IN THE ‘NEW GREAT GAME: CAN PAKISTAN KEEP ITS HOPES HIGH? Spotlight on Regional Affairs .

Benoit Faucon, K. j. (2012). U.S. Redraws World Oil Map:Shale Boom Puts America on Track to Surpass Saudi Arabia in Production by 2020. Wall street journal (online) .

Commission, E. (2013). Energy challenges and policy. European Council.

Deloitte. (2010). Shale gas: A strategic imperative for India.

Dr Arvind Gupta, D. M. (2014). ‘Arab Spring’:Implications for India. New Delhi: Institue of defence studieas and analysis.

El-Katiri, L. (2012). The GCC and Nuclear Question. The oxfor institute for Energy Studies.

(2012). India’s Iran Conundrum: A litmus Test for india's Foreign Policy. HARYANA, INDIA: ASPEN INSTITUTE INDIA.

Ishan Purohit, P. P. (2009). Wind energy in India: Status and future prospects. JOURNAL OF RENEWABLE AND SUSTAINABLE ENERGY .

Jane Nakano, D. P. (2012). Prospects for shale gas development in Asia. Washington: Center for Strategic and International studies: Examining potentials and challanges for China and India.

Khan, A. (2012). IPI pipeline and its implications on Pakistan. Islamabad : Institute of Strategic Studies.

Kumar, D. (2012). Securing India’s Energy Future.

Leena Shirvastva, R. M. (2007). India’s Energy Security. New Delhi: Friedrich Ebert Stiftung.

(2013). Manging Oil wealth. Dubai: AL MASAH Capital Limited.

Parikh, K. S. (2011). The 20th World Petroleum Congress. Doha, Qatar: World Petroleum Congress.

Pradhan, P. K. (2014). India and the Gulf: Strengthening Political and Strategic Ties. In R. Dahiya, DEVELOPMENTS IN THE GULF REGION: Prospects and Challenges for India in the Next Two Decades. New Delhi: PENTAGON PRESS.

Roy, M. S. (2014). India–West Asia Energy Dynamics: Managing Challenges and Exploring New Opportunities. In R. Dahiya, Developments in the Gulf Region: Prospects and Challenges for India in the Next Two Decades. New Delhi: PENTAGON PRESS.

S.K.Jain, D. (2012). Nuclear Power –An alternative.

Ulrichsen, K. C. (2010). The GCC States and the Shifting Balance.

ICSANA - Copyright © 2014. All Rights Reserved.